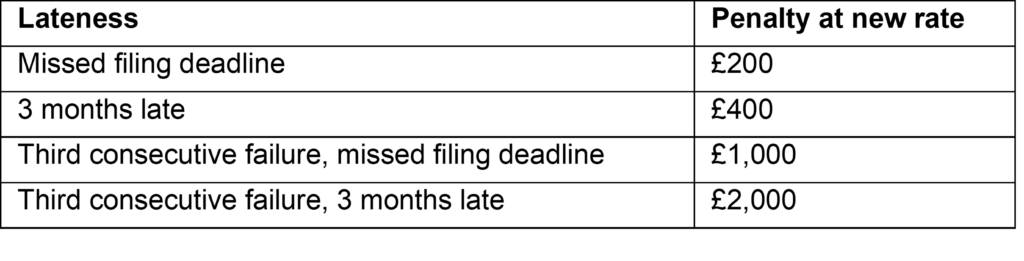

Another key corporation tax change is the new penalty amounts applicable to late-filed corporation tax returns. For returns with a due date that is on or after 1 April 2026, the penalties are:

The CGT rates applicable to gains qualifying for both Business Asset Disposal Relief (BADR) and Investors’ Relief (IR) are set to increase again to 18% on 6 April 2026. The rates previously increased to 14% (from 10%) on 6 April 2025.

VAT

From 1 April 2026, a new relief will exclude most donations of business goods to charities from the deemed-supply VAT rules.